Will the 2024 Presidential Election Move Interest Rates Lower?

With mortgage rates hovering around 7%, housing prices at an all-time high in many places, the question many are asking, “When will mortgage rates go down?” And by go down, most Americans would love to get back to the glory days of sub-4% mortgage rates.

Of course, no one knows for sure when rates will drop significantly or at all, but we can look at history and give a good guess. First, there is a presidential election looming in 2024. In some years, the mortgage rates have come down in presidential election years, while in others it has remained the same or risen slightly. Looking at the data, there doesn’t appear to be a meaningful correlation between presidential elections and mortgage rates. The presidential race will likely not bring mortgage rates down noticeably.

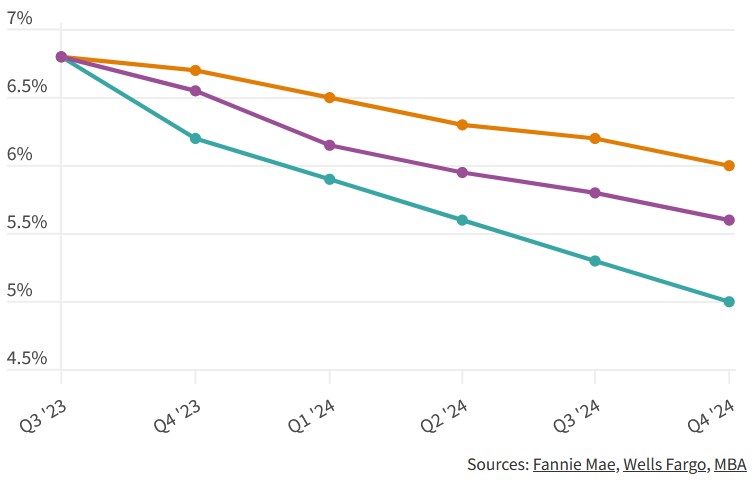

More likely rates are going to be dependent primarily on the economy and inflation. Most economists are now predicting a slowing of inflation but still necessitating a tightening of money by keeping interest rates high. Many outlets including the WSJ and Fannie Mae are predicting a slight decrease in the mortgage rates throughout 2024, but not going below 6%. The days of sub 4% (or even sub 5%) mortgage rates are far, far away… if they ever come back.

I remember my first starter home purchase in 1989. The 12 – 14% interest rates of the late 70’s and early 80’s were still hovering. I was ecstatic with a 9.5% mortgage rate on a $69,000 mortgage. We are all going to have to readjust our expectations. Not to 9.5%, but certainly something higher than 5%. Whether you are a realtor, a mortgage company or a bank, plan on mortgage rates staying in the 6.5% to 7.25% window for the next 12 months. Expect to see more rate buydowns and a return of the assumable rate mortgages… many of which are still available but not utilized. Mortgage refinance activity will increase slightly as Americans run up high interest rate debt, but most will turn to alternative lending options and will leave their first mortgage alone.

I’m not an economist, but our business relies heavily on helping lenders to acquire, retain and cross-sell loans. We are focusing on the increased personal loan activity. In mortgage lenders and banks, the focus is on heavily monitoring current loan portfolios to identify current customers who are in need or who are in the market with loan applications. Also, new purchase activity through pre-listing models (identifying homeowners likely to list their homes soon) and current home listings are driving new home loans. This is what we are seeing and planning for in the coming year. Hope it helps you to plan your business. If I’m wrong, we will all be pleasantly surprised!