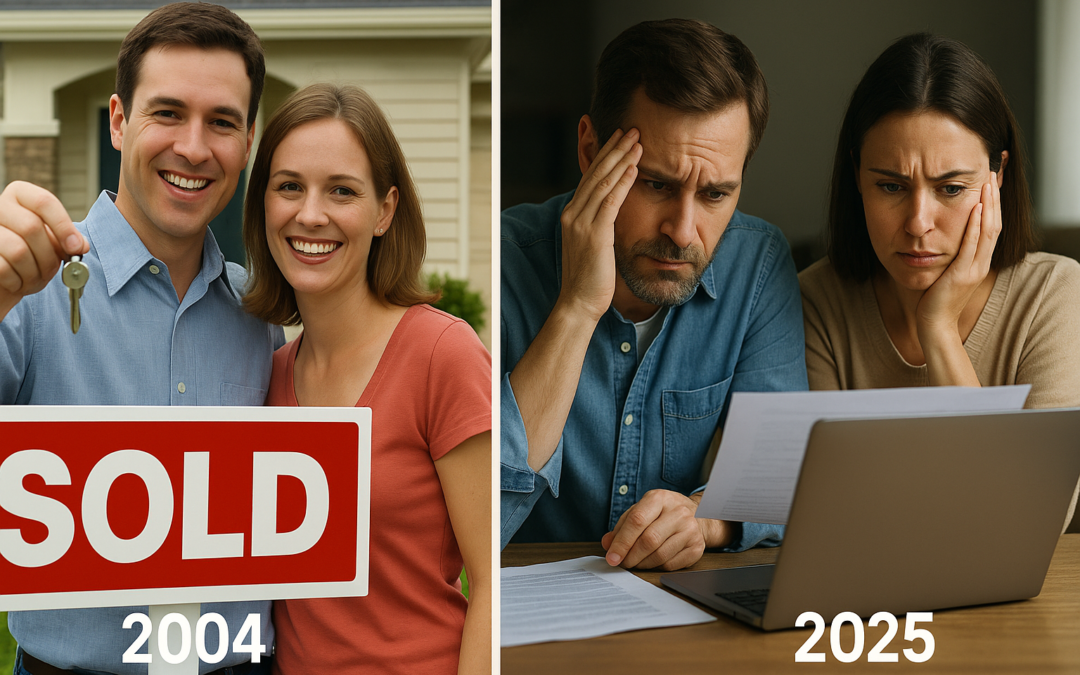

The American Dream of homeownership has become dramatically more challenging for first-time buyers, with striking differences between the housing boom of 2004 and today’s constrained market.

The Bottom Line: A Generation Delayed

The most startling transformation in the American housing market over the past two decades isn’t just about prices—it’s about who can afford to buy and when they can afford to do it. Today’s first-time homebuyers are older, wealthier, and represent a smaller share of the market than ever before recorded.

The Numbers Tell the Story

Market Share: Shrinking Opportunity

2004: First-time buyers comprised approximately 40% of all home purchases during the height of the housing boom, representing a robust entry point for new homeowners.

2025: First-time buyers represent just 24% of all home purchases—the lowest percentage since the National Association of Realtors began tracking this data in 1981.

This 40% decline in market share represents more than statistics; it reflects a fundamental shift in who can access homeownership in America.

Total Numbers: The Dramatic Decline

Perhaps even more striking than the percentage decline is the absolute drop in first-time homebuyer numbers:

2004: Approximately 3.2 million Americans bought their first home during the housing boom year.

2025: An estimated 1.4 million Americans are expected to become first-time homeowners.

This represents a staggering 56% decline in the total number of first-time homebuyers—1.8 million fewer Americans achieving homeownership for the first time compared to two decades ago. This dramatic reduction occurs despite population growth, highlighting how much more difficult first-time homebuying has become.

Age: The Decade-Long Wait

2004: The typical first-time homebuyer was around 31-32 years old during the housing boom years (2003-2006).

2025: The median first-time homebuyer is now 38 years old—a full 6-7 years older than their 2004 counterparts.

This dramatic age increase means today’s first-time buyers have been out of high school for 20 years but are only 24 years away from early Social Security eligibility. They’re buying homes closer to middle age than young adulthood.

Income Requirements: The Wealth Gap

2004: Specific income data from 2004 is limited, but homebuying was generally more accessible to middle-income families during this period.

2025: The typical first-time buyer now has a median household income of $97,000, representing a $26,000 increase just in the past two years. This income requirement has effectively priced out many potential buyers who would have qualified in 2004.

What Changed: The Perfect Storm

Housing Prices: The Great Acceleration

The most obvious difference is cost. Home prices have nearly doubled since 2004, rising from approximately $212,700 to $420,800 today. This 98% increase far outpaced wage growth, creating an affordability crisis that didn’t exist two decades ago.

Interest Rate Rollercoaster

While 2004 had relatively stable mortgage rates, today’s buyers face the aftermath of historically low pandemic-era rates (around 2.96% in 2021) followed by a sharp spike to over 7% in 2025. This volatility has created a “rate shock” that keeps many potential buyers on the sidelines.

Competition from Cash Buyers

One of the most significant changes is the rise of cash buyers. In 2025, 26% of all homebuyers paid cash—an all-time high. These are predominantly repeat buyers with substantial home equity from previous property appreciation, creating intense competition for first-time buyers who typically need financing.

The Inventory Crisis

Unlike 2004’s robust construction activity during the housing boom, the current market faces a severe shortage of approximately 4 million homes. Limited inventory has created bidding wars that favor cash-rich repeat buyers over first-time purchasers.

The Human Impact: Delayed Dreams

Living Arrangements

Today’s housing market has fundamentally altered American living patterns. Young adults are staying in family homes longer, with 25% of younger millennials moving directly from a family member’s home to their first purchase. This “failure to launch” wasn’t as common in 2004 when homeownership felt more attainable at younger ages.

Family Formation

The delay in homebuying correlates with delayed family formation. When first-time buyers were in their early 30s in 2004, they were making these major life decisions—marriage, children, homeownership—simultaneously. Today’s 38-year-old first-time buyers are often established in careers and relationships but have been locked out of homeownership by economic barriers.

Geographic Mobility

First-time buyers in 2025 are moving much farther to find affordable homes—a median distance of 50 miles from their previous location, compared to more localized purchases in 2004. This trend reflects the stark reality that affordable housing often means leaving desirable urban areas entirely.

The Demographic Shift

Relationship Status

2004: The vast majority of first-time buyers were married couples, reflecting traditional family formation patterns.

2025: Only 50% of first-time buyers are married couples (down from 75% in 1985), while 19% are single women, 18% are unmarried couples, and 10% are single men. This diversification reflects broader social changes but also suggests that traditional dual-income married couples no longer dominate first-time buying.

Educational Attainment

Today’s first-time buyers are significantly more educated than their 2004 counterparts, with 78% of younger millennials holding at least a bachelor’s degree. However, higher education hasn’t translated to easier homeownership access—if anything, student loan debt has become an additional barrier.

What This Means for the Future

The Wealth Divide

The data reveals a housing market increasingly divided between the “haves” and “have-nots.” Existing homeowners benefit from equity appreciation and can leverage that wealth for subsequent purchases, while first-time buyers face ever-higher barriers to entry. The reduction from 3.2 million to 1.4 million first-time buyers annually means that 1.8 million fewer households each year are beginning their wealth-building journey through homeownership.

Policy Implications

The dramatic changes between 2004 and 2025 suggest that market forces alone cannot restore first-time buyer access. The situation may require targeted policy interventions, from zoning reform to increase housing supply to first-time buyer assistance programs that address the current reality of $97,000 median income requirements.

The Next Generation

If current trends continue, homeownership may become even more concentrated among older, wealthier Americans. As one industry expert warned, “Give it another 20 years and literally no young person will be able to afford to purchase a home, period.”

Conclusion: A Market Transformed

The comparison between 2004 and 2025 reveals more than changing numbers—it shows a fundamental transformation in American homeownership. What was once a rite of passage for young adults has become a privilege reserved for older, wealthier buyers. The dramatic decline from 3.2 million to 1.4 million first-time buyers annually represents not just individual disappointment, but a systemic failure to maintain the accessibility that defined the American Dream for previous generations.

The housing boom of 2004, despite its eventual collapse, offered genuine opportunities for first-time buyers to enter the market. Today’s constrained market presents formidable challenges that may require unprecedented solutions to restore the accessibility that defined the American Dream for previous generations.

For policymakers, industry professionals, and aspiring homeowners, understanding these changes isn’t just about nostalgia for easier times—it’s about recognizing how profoundly the market has shifted and what it will take to create pathways to homeownership for future generations.

The data in this analysis comes from the National Association of Realtors, Federal Reserve economic data, and various real estate industry reports tracking homebuyer behavior from 2004 to 2025.