“Changes are coming” — Daughtry

Since 2019, we’ve seen an end to a war, a global pandemic, a massive increase in government spending, increased interest rates, home inventory shortages and inflation. The effects of these events have shifted the lending markets dramatically.

Mortgages quickly went from an all-time high, record-breaking refinance boom, to layoffs and some of the toughest conditions mortgage originators have ever seen. While some mortgage lenders have been able to weather the storm by getting creative with rate buydowns and new purchase programs, some have pivoted to home equity loans while others have exited the business for the more economic friendly confines of the personal loan industry.

Yes, you heard that right. Many long-time mortgage professionals have thrown in the towel on mortgage lending and are switching careers to the unsecured lending boat.

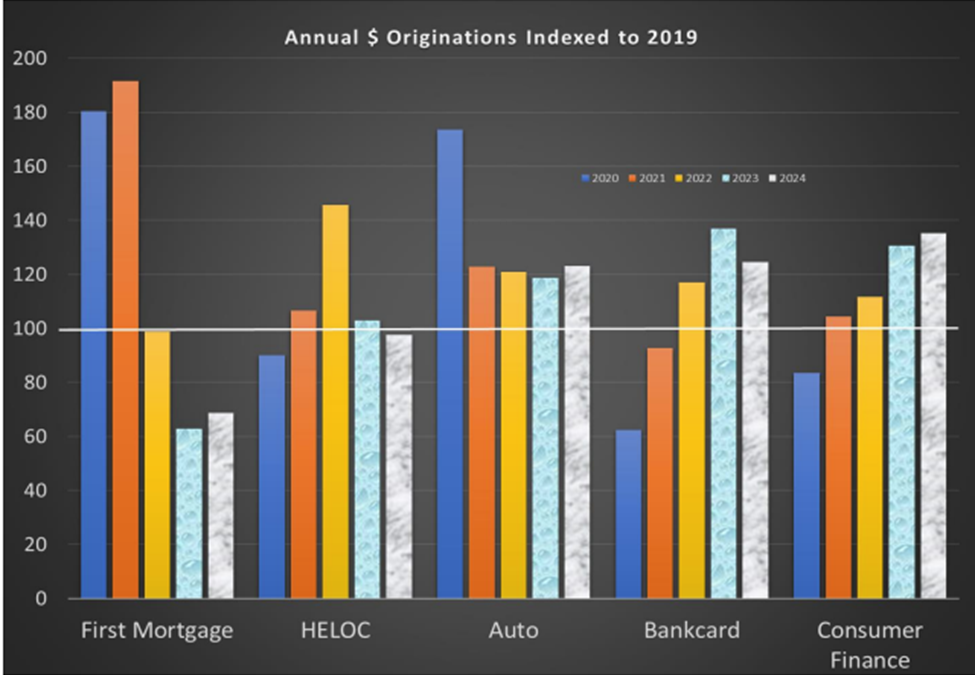

If you want to know why, just check out the graph above. Consumer Finance is steadily growing while HELOC and First Mortgage lending is much less steady, even dropping. Also, the Wall Street journal and others are now referencing treasury bond rates, the fed fund rate, and US monetary policy and inflation as indicators that the mortgage rate will likely remain above 7% well into 2024.

History does tell us that mortgage rates drop in a presidential election year but there are unprecedented conditions that may break that trend in 2024. Plan accordingly!